The 2035 Retrospective

By Sunil Grover, Managing Partner, G2C Ventures

What the Crowd is Missing About the Future of Work!

I’ve been reflecting on the macro shifts coming out of the Acadian Ventures Summit 2026 in San Diego. The room — anchored by Jason Corsello , Thomas Otter , Audrey Handem , and the Acadian team — unanimously agreed on a profound premise: the century-old industrial blueprint of work is being fundamentally re-engineered.

Today, we are officially entering the era of the agentic workforce, where software agents execute end-to-end workflows alongside humans. As the Acadian manifesto puts it: “Execution is no longer scarce — intelligence and clarity are.”

But as a venture investor looking past immediate marketing hype, the path forward is much less smooth, and far more operationally complex, than Silicon Valley admits.

The insights from the panels, case studies, and debates map out the real architectural blueprint of this transformation. And right now, three macro conversations are dominating the serious rooms in venture — not the keynote stages, but the hallway debates and LP calls where the real theses get formed.

The first is whether SaaS can hold its moat. Foundation models keep improving, absorbing what used to be defensible product territory. The SaaS companies that survive won’t be the ones with the best demos — they’ll be the ones with proprietary data pipelines, deep workflow integrations, and switching costs so high that leaving would break their customer’s operations entirely.

The second is what the unprecedented concentration of VC into AI actually means for founders. When 65% of global venture deal value flows into a single category, capital stops being a differentiator and becomes a gatekeeper. The funding bar hasn’t lowered — it has simply moved. Non-AI-native companies are being systematically de-prioritized, while AI founders who can show genuine workflow depth and real enterprise contracts are raising at terms that would have seemed impossible two years ago.

The third — and the one that ties everything together — is the rise of agentic AI embedded directly into vertical workflows. Not AI as a feature bolted onto existing software, but AI as the operating layer of an entire industry function. This is the investment thesis that serious capital is quietly building around, away from the noise.

If we look back at today from the vantage point of 2035, (thanks Matthew McCooe ) what will we realize we completely missed? The insights from the panels, case studies, and debates map out the real architectural blueprint of this transformation.

1. The Reality Check: AI is a Circular Saw, Not a Railway

Every major tech wave is compared to the steam engine or the expansion of the railway system—macro infrastructure where everyone just hitches a ride and moves forward together.

But as Acadian General Partner Thomas Otter highlighted during the summit, AI may not be a railway. It’s a circular saw.

It is an incredibly powerful, highly localized, and dangerous power tool that demands specific mastery. Right now, the enterprise market is split into three tiers:

- The Tourists: The massive wave buying the saw, building a basic “wrapper” project, and letting it sit in the garage.

- The Casualties: Overconfident enterprises rushing into implementation without guardrails, “cutting their fingers off” via data leaks and compliance blunders.

- The Craftsmen: A small, highly skilled fraction of the marketplace taking the time to master the tool to achieve astronomical levels of efficiency.

2. The Billion-Dollar Proof: From Deflection to Extension

True craftsmanship is not about cutting headcount to save OpEx. David Wright (Chief Innovation Officer at ServiceNow) shared a gold-standard case study during the sessions: IKEA.

IKEA deployed an AI agent named “Billie” that successfully automated 57% of customer support inquiries. Instead of treating this as a cost-cutting cue to slash headcount, IKEA took 8,500 customer service reps and upskilled them into Remote Interior Design Consultants.

By automating cold execution, they liberated human creativity. That single pivot turned a traditional cost center into a massive growth engine, generating $1.4 billion (€1.3B) in net-new revenue in its first year. That is the ultimate validation of shifting from a System of Record to a System of Outcomes.

3. The Enterprise Battleground: P&L Warfare and Portable Intelligence

Despite the IKEA success story, the path to enterprise adoption is hitting a corporate wall. The structural reality of the enterprise tech stack relies on five layers: Infrastructure, Intelligence, Automation, Experience, and Compliance. Yet, a silent boardroom war is brewing over who actually owns the “Agentic P&L.”

Historically, enterprise tech shifted from CapEx to OpEx (SaaS licenses). Today, token and compute costs are scaling so rapidly that they can no longer be hidden under an IT utility bill—they are a direct replacement for human capital. As industry leaders like Gretchen Alarcon (UKG) and former Disney CHRO John Renfro debated behind the scenes, this reality fractures traditional corporate governance:

- Does the CIO procure the agent because it’s deep-tech?

- Does the COO fund it because it drives operational output?

- Does the CHRO onboard it because it is executing a human job function?

Compounding this is the compliance nightmare of BYOA (Bring Your Own Agent). Top-tier professionals do not want to join a company as a single individual; they arrive as a “Human + Agent” unit, carrying their personal, pre-trained workflow memory with them. If a company forces a craftsman to leave their personal circular saw at the door, their productivity will collapse. But how do CISOs protect corporate IP when that agent leaves for a competitor?

4. The Chokepoint of Data

For these agents to deliver business outcomes, they need fuel. And that fuel doesn’t live on public LLMs; it sits deep within legacy mainframe ERP systems.

As Ognjen Pavlovic (Oracle) and Josh Gosliner (SAP) reflected at the infrastructure of enterprise data, the audience wondered whether the software landscape will be determined by how these legacy incumbents guard their data chokepoints?

- Will they act like the Strait of Hormuz? Choking the flow of data, holding information hostile, and demanding a ransom to protect their legacy turf?

- Or will they act like the Panama Canal? Recognizing traffic must flow, and focusing on creating massive revenue through efficient, regulated toll passage?

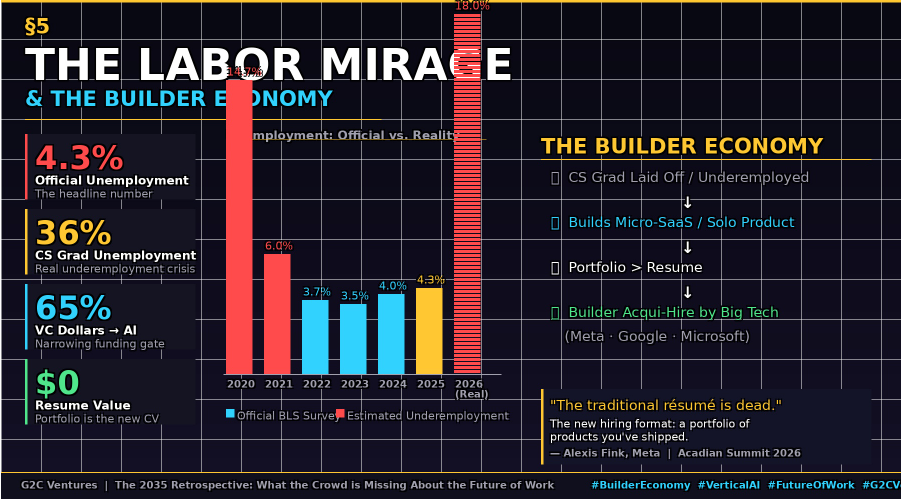

5. The Labor Mirage and the Builder Economy

While these enterprise wars rage, macro data may be lying to us. The official 4-5% unemployment rate is a statistical mirage driven by outdated landline phone surveys.

Did you know that if a laid-off Computer Science graduate or a recent CS grad looking for a job (36% umemployment rate) drives an Uber for a few hours to pay rent, they are labeled “fully employed?” So what does a 4.3% unemployment rate mean when all GDP growth is driven from investments in capital intensive datacenter infrastructure.

In reality, we may have a massive technical underemployment crisis. But these stranded builders aren’t waiting around; backed by platforms pushing real-time talent dynamics like Charlie Franklin (Compa) and global workforce models like Eynat Guez (Papaya Global) and Tony Jamous (Oyster), we are witnessing the explosive growth of solo ventures and independent micro-SaaS tools.

Big Tech has already noticed. Companies like Meta (Alexis Fink) and Google are shifting entirely toward acute hiring. The traditional resume is dead. The new format for elite hiring is a portfolio of products you’ve built, resulting in a wave of “Builder Acqui-hires” where corporations buy the solo product just to bring the builder’s talent and velocity in-house.

6. The 2035 Retrospective: The “Last-Mile” Brittle Point

This brings us back to the brilliant question posed by Matt McCooe (CEO of Connecticut Innovations): Looking back from 2035, what did we miss?

The biggest macro mistake investors are making today is overestimating the speed of enterprise adoption and assuming AI will break the historical laws of global GDP (which has normalized at ~2% for a century). AI won’t magically double global GDP; it will radically disrupt where that 2% is captured.

Enterprise adoption will move far slower than anticipated because of The Last-Mile Brittle Point.

Think of Waymo. Cracking 90% of autonomous driving happened fast. It required controling four degrees of motion. Forward, back, left and right. But patching the final, brittle 1% of edge-case reliability to earn absolute human trust took ten years and billions of dollars. Enterprise AI is hitting that exact same wall. A 1% failure rate in a corporate compliance or financial agent can destroy an enterprise. Because fixing this last mile is incredibly capital-intensive, the smart capital isn’t going to flash-in-the-pan wrapper apps—it is flowing directly to the Infrastructure of Work (the foundational plumbing, validation, and guardrail layers built by pioneers like Aaron Matos at Paradox and Chris Bruce at Origin).

The Generational Opportunity: Backing the Titans of 2035

When we look back at today from the vantage point of 2035, the biggest unexpected revelation won’t be a technological breakthrough in large language models or physical AI—the emergence of massive winners in those fields is already a given. Instead, the true surprise will be the staggering triumph of founder conviction—the unique resolve to build entirely new industries that fundamentally reimagine both the workflows and the business models of traditional legacy sectors.

While the friction of tackling these massive market opportunities can entice teams and their investors toward early, comfortable $500M exits, the true winners of this decade will be the visionary leaders who possess the nerve to ride the wave all the way through. By holding out for generational scale, these resilient teams will transform today’s brightest startups into the $100B category-defining titans of tomorrow. That, I believe, is the ultimate vision we are still missing today.

Closing thoughts…

At G2C Ventures, we approach this shifting frontier with an Abundance Growth Mindset. We don’t view venture capital as a zero-sum game; we actively collaborate with leading VCs like Acadian—investing as LPs in their funds and welcoming them into ours—because cross-pollinating intelligence is the ultimate way to architect this new ecosystem.

The technology is changing at breakneck speed, but the core fundamentals of venture success remain entirely unchanged: robust unit economics, strategic distribution, deep enterprise trust, and the unwavering courage to build for the long horizon. At G2C Ventures, we are here to back that exact endurance.